Immediately, we current a visitor submit written by Charles Engel, Donald D. Hester Distinguished Chair in Economics at UW Madison and Steve Pak Yeung Wu, Assistant Professor of Economics at UCSD.

It’s typically believed that normal macroeconomic empirical fashions of international change charges don’t match the information properly. (See for instance, Meese and Rogoff (1983), Cheung, et al. (2005), and Itskhoki and Mukhin (2021).) Nevertheless, we discover that these fashions match very properly for the U.S. greenback within the 21st century. A “normal” mannequin that features actual rates of interest and a measure of anticipated inflation for the U.S. and the international nation, the U.S. complete commerce stability, and measures of world threat and liquidity demand is well-supported within the information for the U.S. towards different G10 currencies. The “financial variables” (that’s, actual rates of interest and anticipated inflation) and non-monetary variables play equally vital roles in explaining change price actions. Within the Seventies – early Nineties, the match of the mannequin was poor, however the mannequin efficiency has improved steadily to the current day. We make the case that it’s higher financial coverage (inflation concentrating on) that has led to the development, because the scope for self-fulfilling expectations has disappeared. We offer quite a lot of proof that hyperlinks adjustments in financial coverage to the efficiency of the exchange-rate mannequin.

The hyperlink to the working paper is right here. This notice leaves out the technical particulars and references to the literature, that are within the paper. We look at the determinants of the greenback relative to the euro, the U.Okay. pound, the Canadian greenback, the Australian greenback, the New Zealand greenback, the Norwegian krone, and the Swedish krona. The Japanese yen and Swiss franc are particular circumstances which we handle individually.

The empirical mannequin hyperlinks adjustments in bilateral month-to-month change charges to:

- Actual rates of interest within the U.S. and the “international” nation. Most macro fashions of change charges posit {that a} greater actual rate of interest induces a stronger foreign money. A rise within the U.S. actual rate of interest leads the greenback to understand, and the next international actual rate of interest is related to a greenback depreciation.

- Inflation. Maybe paradoxically, greater inflation within the U.S. ought to result in a greenback appreciation (and better international inflation to a greenback depreciation.) That is the conclusion of the New Keynesian macroeconomic paradigm when financial coverage is credible. Larger inflation (over the previous 12 months) leads central banks that focus on inflation to tighten. Since we already management for actual rates of interest, that are decided by the present stance of financial coverage, this channel captures expectations of future financial coverage actions.

- Commerce stability on items and providers within the U.S. Because the commerce deficit will increase, the U.S. internet international asset place deteriorates. Particularly within the early 21st century, markets grew to become involved that insurance policies can be undertaken to weaken the greenback to cut back the worth of exterior debt, so greater commerce deficits are related to a depreciating greenback.

- International threat. The greenback is taken into account a “safe-haven” foreign money. Throughout instances when international threat is excessive (as measured right here by bond market spreads), the greenback strengthens.

- Liquidity. Additionally, throughout instances of world stress, markets improve demand for greenback liquid belongings. As that demand rises, the “comfort yield” on U.S. Treasury belongings will increase, and the greenback appreciates.

- Buying Energy Parity. When the relative buying energy of the greenback may be very misaligned, there’s a (weak) tendency to return to the PPP stage.

Mannequin Estimation

The mannequin is estimated currency-by-currency and in addition collectively by panel estimation. The macro variables typically have the signal and magnitude per financial principle and are often fairly statistically important when estimated over the January 1999 to August 2023 interval. (The start line right here is chosen as a result of it corresponds to the arrival of the euro.) Determine A proven right here plots the “fitted values” of the mannequin towards the precise change price.

Particularly, because the mannequin is estimated for the month-to-month change within the change price, the fitted worth for the degrees that’s plotted right here cumulates the mannequin’s estimated change every month to supply the mannequin’s match for the extent of the (log of) the change price. The preliminary worth within the cumulation is chosen to make the general common of the fitted values equal the general common within the information.

One factor to be very clear about right here is that we aren’t forecasting change charges. The empirical mannequin makes use of information from, for instance, January 2000 to clarify the January 2000 change price. Even when the macroeconomic fashions of change charges are good fashions, they most likely usually are not helpful fashions for forecasting. Principally, change charges change from month to month due to unanticipated adjustments in explanatory variables. However these unanticipated adjustments can’t, by definition, be forecast, so forecasting the change in change charges turns into very tough even with the very best mannequin in hand.

The Mannequin Matches

Turning to Determine A, taking the euro change price for instance, the fitted values reproduce properly the preliminary appreciation of the U.S. greenback from 1999-2000, adopted by the depreciation of the U.S. greenback from 2001 to 2008. The fitted collection additionally matches the sharp appreciation of the U.S. greenback in 2008, 2010, and 2013. Each the information and the fitted collection exhibit an appreciation of the greenback from 2013 onwards. The model- implied collection additionally suits the sample post-2020 very properly, mimicking the V-shape from 2021 to 2023. The shut correspondence between the crimson line and the blue strains holds for all different currencies in numerous sub-periods between 1999 and 2023.

Determine A: Evaluating information and mannequin implied change charges

The Match has Improved over Time

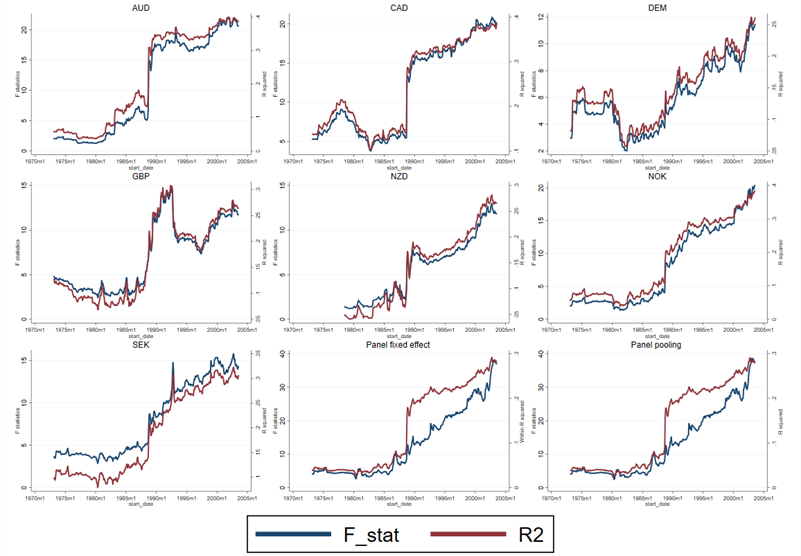

However the mannequin didn’t match over earlier samples. We doc this by estimating the mannequin over 20-year rolling samples starting in 1973. Within the earlier samples, the match was poor – the variables are often statistically insignificant; typically when they’re important, they’ve the unsuitable signal; and the R-squared values are low. F-tests of the joint significance of the explanatory variables fail to reject the null. However there’s a near-monotonic improve within the F-statistics and R2s because the samples progress in time, and these statistics primarily attain their most within the ultimate 20-year pattern. Determine B plots the R-squared and F statistics over time from these rolling regressions. It exhibits that the fashions match poorly within the early samples, however that the match has steadily improved.

Why the Mannequin Didn’t Work within the Outdated Days

What accounts for the poor match of the fashions within the ancient times, and the wonderful match now? We argue {that a} change in financial regime could clarify this. As we present, financial principle implies that when central banks don’t comply with a reputable inflation-targeting coverage, there may be scope for self-fulfilling expectations to affect variables within the financial system, together with inflation, output, and change charges. Intuitively, suppose markets conjure up a perception that inflation can be greater. If central banks don’t reply forcefully sufficient to this modification in expectations, actual rates of interest will fall. That may stimulate combination demand, result in inflation and a weaker foreign money. We contend that as credibility elevated, this phenomenon decreased, and the match of the usual mannequin improved. When financial coverage is credible, an expectation of inflation whipped up out of skinny air is not going to be sustained as a result of tighter financial coverage will rapidly be seen to eradicate the probability of future inflation.

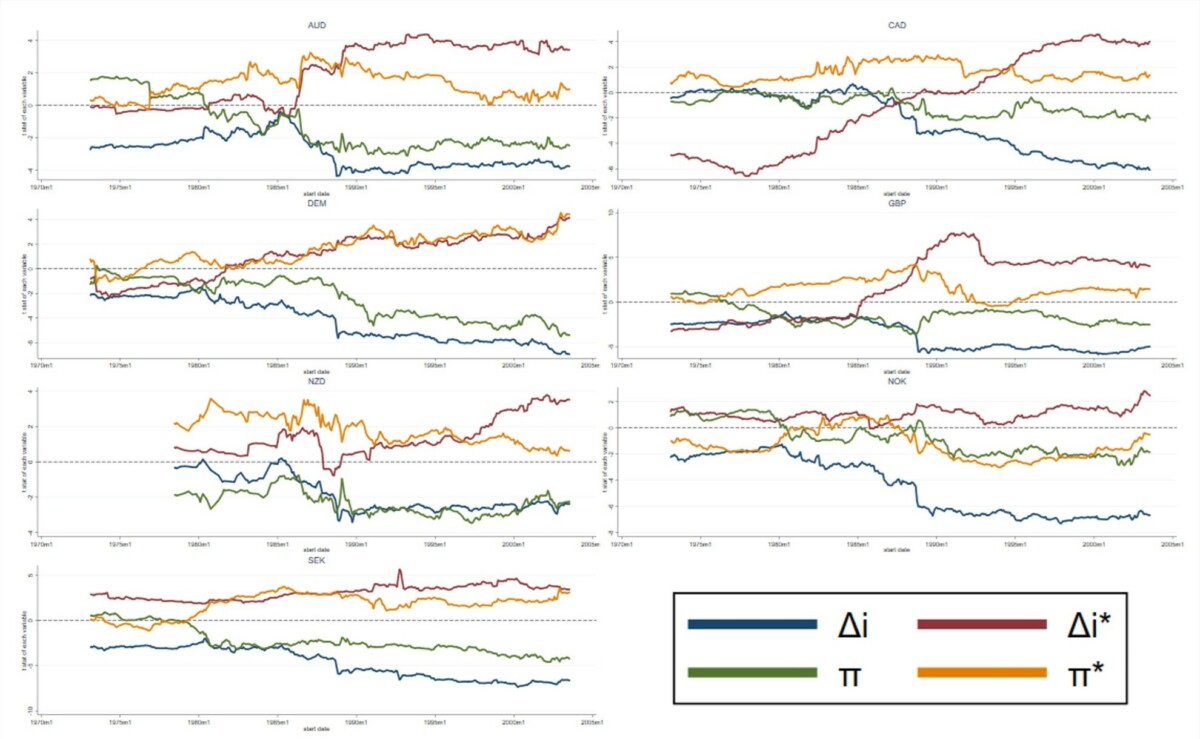

That the development in match is expounded to the financial variables is obvious in Determine C, which plots the t-statistics for the true rate of interest variables (Δi, Δi*) and the measures of inflation (π and π*) from rolling 20-year regressions. The t-statistic measures the contribution of the variable (the estimated regression coefficient) scaled by the precision of the estimate (the inverse of the usual error of the estimate), so it offers us a good suggestion of how vital every variable is in explaining change price actions. In these graphs, if the idea is appropriate, the t-statistics ought to be unfavorable for the U.S. interest-rate and inflation variables and optimistic for the international variables. Values which are above roughly 2.0 are statistically important. We will see from Determine C, with a number of exceptions, that the variables have been hardly ever important within the early a part of the pattern and sometimes had the unsuitable signal, however within the later samples, they’ve the fitting signal and are important.

The rate of interest and inflation variables are vital as a result of they point out whether or not financial coverage change charges are responding to credible financial insurance policies. If insurance policies are credible, greater actual rates of interest ought to make the foreign money stronger, and better inflation ought to sign future insurance policies can be tighter and in addition will admire the foreign money. That sample doesn’t maintain within the earlier samples however does within the later samples.

Determine B: F-statistic and R-squared of 20-year rolling window regressions

Determine C: t statistics of 20-year rolling window regressions

Financial coverage for the U.S. started to shift throughout the Volcker period, in order that Taylor guidelines estimated on information starting within the mid-Eighties supply help for financial stability. The superior international locations in our pattern adopted inflation concentrating on a number of years later: New Zealand in 1990, Canada in 1991, the U.Okay. in 1992, Sweden and Australia in 1993, Norway in 2001. One of many pillars of European Central Financial institution coverage, starting in 1999, is inflation concentrating on. Germany formally adopted inflation concentrating on in 1992 earlier than the arrival of the euro, although concentrating on inflation was at all times on the core of Bundesbank coverage.

The paper produces additional proof to help the shift in financial coverage in these international locations and its gradual growing credibility. The vital contribution right here is that the success of the empirical mannequin doesn’t rely solely on the danger and liquidity variables, that are vital in monitoring the actions of the greenback throughout instances of world monetary stress. The variables that signify the stance of financial coverage within the U.S. and the opposite international locations are key to accounting for the great match of the mannequin immediately and its poor match previously. It’s pure to attribute this modification over time to the altering nature of financial coverage.

Empirical Trade Charge Fashions are Higher than You Assume

Clearly, the match of the mannequin isn’t good. There could certainly be different elements driving change charges, together with non-market “noise buying and selling” that has been emphasised in some latest research. Nevertheless, it’s seemingly {that a} main purpose the match isn’t good is as a result of economists can’t completely measure the variables that principle says ought to drive the change price: the stance of financial coverage, the extent of world threat, the demand for liquidity, and many others. Determine A actually exhibits that the empirical mannequin is ready to seize main elements driving greenback change charges.

This submit written by Charles Engel and Steve Pak Yeung Wu.

{kind=link}