")

Locking up the butter in Russia (CNN). Official inflation in October was 0.8% m/m (annualize that and it’s about 10%. That’s the official inflation price. The ex submit price is round 11% then.

Taking the CBR’s anticipated inflation price of 13.4% at face worth, this suggests a 7.6% ex ante actual price. With the coverage price anticipated to rise to 23% at December’s assembly, this might suggest 9.6% ex ante actual charges assuming anticipated inflation stays fixed.

There’s an attention-grabbing query of whether or not we are able to take the CPI numbers popping out of the Rosstat at face worth. A current report by the Stockholm Institute of Transition Economics observes:

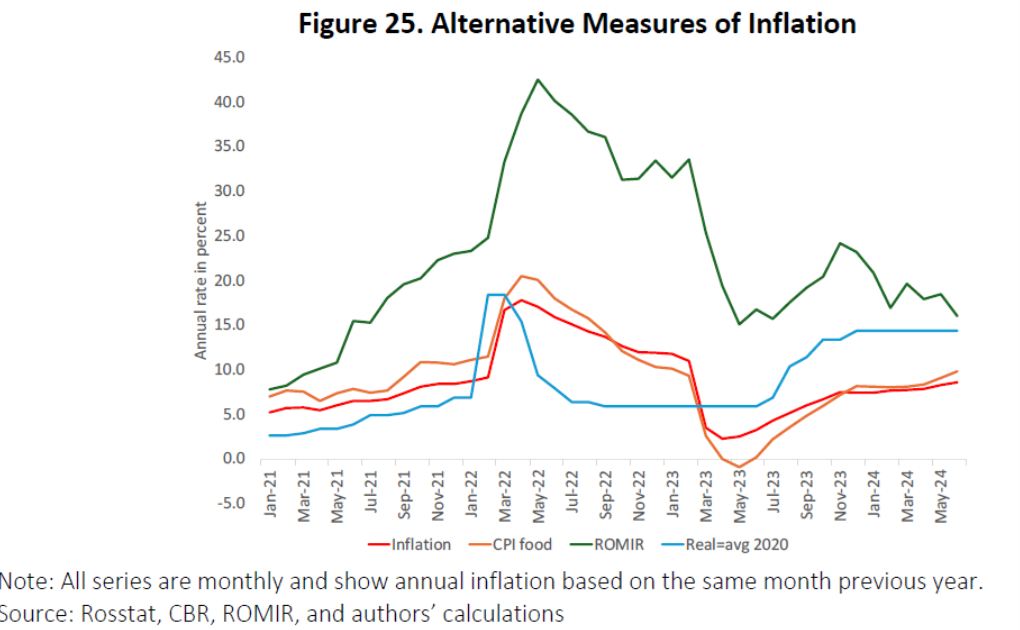

…the credibility of the official inflation numbers put out by Rosstat. Determine 25 reveals some different measures of inflation that counsel that the official numbers might significantly understate the inflation households face. The primary different measure is the fastmoving client items (FMCG) index produced by the unbiased Russian public opinion monitoring service ROMIR.25 The FMCG largely contains meals and cosmetics and ROMIR estimates that the share of FMCG in whole family expenditures is round 50 p.c. Their index produces persistently greater inflation charges than each whole CPI and the meals CPI index produced by Rosstat. In Might of 2022 their inflation measure peaked at over 40 p.c at an annual price. It has since come down considerably however has remained at round twice the charges revealed by Rosstat. In June 2024, which is the newest month at the moment obtainable, the ROMIR inflation price is at 16 p.c versus 8-10 p.c for the CPI and meals CPI inflation by Rosstat. In distinction to ROMIR, Rosstat historically considers the share of meals within the Russian CPI basket to be 38 p.c, which Milov (2022) argues is simply too low and results in an underestimation of inflation. Secondly, Rosstat observes costs for items which shoppers do the truth is purchase. It’s probably that many Russian households have began to purchase cheaper substitute items because of the sanctions and finances constraints and that such substitution results is not going to be mirrored in CPI.

Right here’s Determine 25 from that research.

Supply: Stockholm Institute for Transition Economics.

Determine 25 additionally supplies an implied inflation price if CBR was making an attempt to carry the true coverage price at 2020 ranges. Utilizing that logic to assemble another anticipated inflation sequence is smart if the pure price (r*) doesn’t change. Nevertheless, my guess is that given the massive fiscal stimulus and lack of labor inventory, r* in all probability has modified, so the blue line is especially questionable in my thoughts.

In any case, a 21% coverage price mixed with both 13.4% or 16% (10% official CPI plus 6 proportion factors for mismeasurement) nonetheless yields a 5-7.6% actual price — fairly excessive.

{kind=link}